jedamedia.my.id – The average cost of car insurance is a subject that concerns every driver. Car insurance is not only a legal requirement in most places but also a financial safeguard in case of accidents or other unexpected events. However, many drivers are often confused by how car insurance premiums are calculated and wonder if they are paying too much.

This comprehensive guide delves deep into the factors that affect car insurance costs, shedding light on the ways you can reduce your premiums and find the best coverage for your needs. By understanding the intricacies of car insurance, you can make informed decisions, ensuring your financial well-being while enjoying peace of mind on the road.

Table of Contents

ToggleThe Average Cost of Car Insurance

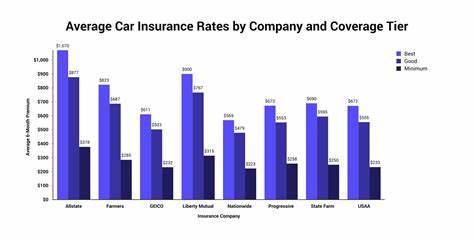

The average cost of car insurance in the United States is around $1,674 per year, which comes out to about $140 per month. However, this number is highly variable and depends on several key factors such as:

- Your Age

- Your Driving History

- The Type of Vehicle You Drive

- Your Location

- Your Chosen Insurance Coverage

Each of these factors plays a significant role in determining your overall car insurance premiums. Let’s take a closer look at how each of these factors contributes to the cost.

Factors That Affect Car Insurance Premiums

1 Age

One of the most significant factors that determine car insurance premiums is age. Younger drivers, especially teenagers and those in their early twenties, tend to pay higher premiums than older drivers. This is because younger drivers are statistically more likely to be involved in accidents, as they typically have less experience on the road.

For example, a driver between the ages of 16 and 19 could pay an average of $2,340 per year for car insurance, while a driver in their 30s might pay closer to $1,240 annually.

2 Driving History

Your driving record is another crucial factor that insurers take into account. Drivers with a clean record, meaning no accidents or traffic violations, are considered low-risk and thus benefit from lower premiums. Conversely, a history of accidents or violations will increase the cost of your insurance.

For instance, if you’ve had two or more accidents, you could be paying significantly more—up to three times the premium compared to someone with a clean driving record.

3 Vehicle Type

The type of car you drive also impacts your car insurance costs. Sports cars, luxury vehicles, and cars with high-performance engines generally cost more to insure. This is because these vehicles are more expensive to repair or replace, and their drivers are statistically more likely to speed or be involved in accidents.

On the other hand, family-friendly vehicles like sedans, minivans, or SUVs are typically cheaper to insure due to their safer design and lower risk profile.

4 Location

Where you live can have a dramatic effect on the price of your car insurance. Drivers in urban areas, where traffic is denser and accidents are more common, generally face higher insurance premiums than those in rural areas. Additionally, states like New York or California tend to have higher average insurance rates due to factors such as the cost of living, frequency of accidents, and even the likelihood of theft.

For example, a driver in New York might pay significantly more for insurance than a driver in a rural area of the Midwest.

5 Insurance Coverage Options

The level of coverage you choose directly affects how much you’ll pay for car insurance. There are generally three levels of coverage to consider:

- Liability Coverage: This is the minimum required by law in most states and is typically the most affordable option. It covers damage or injuries you cause to others but does not cover your own injuries or vehicle.

- Comprehensive and Collision Coverage: This provides more extensive protection, covering your vehicle in case of accidents, theft, natural disasters, and vandalism. As this type of coverage offers more protection, it also comes with higher premiums.

- Uninsured/Underinsured Motorist Coverage: This protects you if you’re involved in an accident with a driver who either doesn’t have insurance or doesn’t have enough coverage to pay for the damage. Including this in your policy can increase your premiums, but it provides additional peace of mind.

The more comprehensive your coverage, the more you will pay, so it’s essential to evaluate your needs carefully.

Average Cost of Car Insurance by Age and Driving History

The table below gives an overview of average annual insurance premiums based on age and driving history.

| Age Group | Clean Driving Record | One Accident | Two or More Accidents |

|---|---|---|---|

| 16-19 | $2,340 | $4,680 | $7,020 |

| 20-24 | $1,820 | $3,640 | $5,460 |

| 25-29 | $1,460 | $2,920 | $4,380 |

| 30-34 | $1,240 | $2,480 | $3,720 |

| 35-39 | $1,120 | $2,240 | $3,360 |

| 40-44 | $1,020 | $2,040 | $3,060 |

| 45-49 | $940 | $1,880 | $2,820 |

| 50-54 | $880 | $1,760 | $2,640 |

| 55-59 | $820 | $1,640 | $2,460 |

| 60-64 | $780 | $1,560 | $2,340 |

| 65+ | $740 | $1,480 | $2,220 |

As shown, the cost of insurance rises significantly for younger drivers and for those with accidents on their record.

How to Compare Car Insurance Quotes

To find the best deal on car insurance, it’s essential to compare quotes from multiple providers. While comparing quotes, keep the following factors in mind:

- Coverage Limits: Ensure that the coverage limits meet your needs.

- Deductibles: Higher deductibles result in lower premiums, but you’ll need to pay more out-of-pocket if you file a claim.

- Financial Strength of the Insurer: A financially strong insurance company is more likely to be able to pay out claims quickly.

- Customer Service Ratings: Good customer service ensures a smoother experience if you need to make a claim.

It’s a good practice to request at least three quotes before deciding on a provider.

Tips to Reduce Car Insurance Costs

If you’re looking to lower your car insurance premiums, consider the following strategies:

- Maintain a Clean Driving Record: The fewer traffic violations or accidents you have, the lower your premium will be.

- Take Defensive Driving Courses: Many insurers offer discounts to drivers who complete defensive driving courses.

- Install Safety Features: Adding safety features such as anti-theft devices, airbags, and automatic braking systems can help reduce your insurance rates.

- Raise Your Deductible: Increasing your deductible can significantly lower your premium. However, make sure you can afford the deductible in case of an accident.

- Bundle Insurance Policies: Many insurance companies offer discounts if you bundle your car insurance with other policies, such as homeowner’s or renter’s insurance.

Epilogue: Understanding the True Cost of Car Insurance

In conclusion, understanding the true cost of car insurance requires more than just looking at the price tag. It involves evaluating various factors such as age, driving history, vehicle type, and location. By carefully considering these elements and comparing quotes, you can ensure that you get the best possible coverage for your needs without overpaying.

Remember, car insurance is more than just a monthly expense—it’s an essential part of financial security, offering protection for you, your passengers, and your vehicle in case of unexpected incidents.

Making informed decisions about your coverage will not only save you money but also provide the peace of mind that comes with knowing you’re adequately protected.

{kind=link}